We’ve been covering “FedNow” for a long time here at WLTReport….since probably before you even knew what it was, or had ever heard of it.

Now it’s starting to hit the MSM.

Yesterday, I did a huge post explaining exactly what happens when FedNow launches and why it will be bad — VERY bad — for privacy and for censorship.

I’ll repost that down below if you missed it, but first an update…

It was previously expected that FedNow was launching July 1.

By all available sources, that has now been revised to July 20.

Take a look:

Federal Reserve just updated their website home page. #FEDNOW

July 20th – "The Magic Day" <–#Finastra pic.twitter.com/LhDveNuqVX

— Chad Steingraber (@ChadSteingraber) July 1, 2023

—1 DAY—

Countdown to history as #FEDNOW goes 🟢

June was final testing and certification – meaning every member had to fully compliant.

CERTIFIED— -Finastra ✅ -Volante ✅ -ACI Worldwide ✅ -CGI ✅

“CLOSED BETA” BEGINS on REAL transactions ✅

JULY 20th is “The Magic Day” ✅ https://t.co/WpCJPVECv7

— Chad Steingraber (@ChadSteingraber) June 30, 2023

There are 57 participating early adopters in the “Closed Beta”:

-TODAY-

History has been made as ALL pilot participants have certified!✅#FEDNOW has the 🟢💡

“Closed Beta” begins as all certs must run LIVE REAL WORLD tests to verify their readiness and confirm actual transactions.

PROVIDERS are 🟢#RippleNet is 🟢

July 20th – Magic Day pic.twitter.com/j3WNiqQMVy

— Chad Steingraber (@ChadSteingraber) July 1, 2023

It all officially goes live July 20:

So, when does #FedNow go live exactly? We know, based on FedNow docs that it is July 2023. But until now that's all we knew. It appears #FedNow will go live July 20, 2023 according to Kristin Robertson, Director at #Finastra. #Ripple #XRP #XRPArmy #XRPHolders pic.twitter.com/agkyO7gWQh

— Crypto Investment Group (@CryptoIG_) June 29, 2023

Now for the BIG questions….

For those who missed it, I’ll tell you exactly what is coming next…and why it’s so bad.

Here’s What Happens When FedNow Goes Live…

I’ve been getting a lot of questions recently from people asking me “What happens when FedNow goes live?”

Even some family members reaching out.

So I thought I’d address it.

Short answer?

No one really knows for sure, because this is new unpaved ground.

We’ve never done this before.

But I think I have a pretty good idea of where it’s going so let me break it down for you.

FedNow is the new system designed to roll out the U.S. CBDC, which stands for Central Bank Digital Currency.

Central Bank = The Federal Reserve Bank = “The Fed”

And as a friendly reminder, the Federal Reserve Bank is:

Not Federal (it is entirely ran by private, Deep State families)

Not A Bank

Has No Reserves

Imagine that…even in the name, they lied to you three times!

So The Fed now wants to go digital.

Why?

Control.

Right now, when you have cash or even your bank accounts at local banks or credit unions, The Fed doesn’t have great control over what you do with that money.

But….if the money were digital and if the connection was made directly between YOU and The Fed, then suddenly they can exert a ton of control over you.

You know how you get locked out of Facebook if you say the wrong thing?

Now imagine that happening to your bank account.

Posted the wrong thing online?

Used the wrong pronoun?

Had a wrong thought?

Sorry, you just got zapped by FedNow!

Your money is now inaccessible for 24 hours.

Sure hope you don’t have another violation, next freeze out will be 7 days.

Third violation?

One month strike!

Think that can’t happen?

It can, and it’s coming.

But that’s not all.

No, this will be “programmable money” which means it’s very different than cash.

With cash, you can choose to spend it however you want.

Buy groceries, take a trip, gamble it away….you choose!

Some decisions are smarter than others, but YOU have always been in control of that decision for YOUR money.

Not anymore.

Federal CBDC programmable money means The Fed can put restrictions on what you can do with it….and it all goes right into the computer code!

So sure, maybe you have $5,000 in your account, but shoot….the overlords at The Fed have noticed you’ve been traveling too much recently.

Taking too many plane trips…

You’ve been flagged as a polluter!

Your money is now locked out for 6 months from being allowed to be used for anything related to travel.

Hope you like staying home!

Think that can’t happen?

It can, and it’s coming.

Now, watch how they try to spin this…

They’ll say, no, no, that’s not true!

What Noah is telling you is a lie….

They’ll do “Fact Checks”.

They’ll roll out all their buddies at all the big Fact-Checking websites and they’ll deem what I just told you 100% FAKE — NOT TRUE, they will say!

Why?

Because they’ll say FedNow is not a direct link from The Fed to your bank account.

You don’t have a direct account with The Fed.

You still have your account at your local bank.

So see?

See….we can’t control your money because there’s still a bank in between us and you!

So nothing to worry about.

So devious.

That’s how they always do this stuff.

They boil the frog SLOWLY.

Same game plan they’ve been running for years.

They’re going to get you used to this system exactly that way, by saying there’s really nothing new here, you still have your account at your local bank or credit union, and The Fed has no direct control over you.

And they’ll be right….for now.

But for those of you paying attention and reading along with me, you’ve already connected the dots in your head on what comes next, right?

What is the final step they need to remove that last barrier?

Remove the local banks, of course!

And gee, what did we see back in April and May of this year?

A banking crisis where in the span of 3 days we lost four huge banks!

Just gone — poof, overnight!

Went to zero!

Absorbed into JP Morgan Chase.

The big get bigger and the small(er) banks disappear.

Was that….a test run?

I think so.

They tested out how quickly they could take down a bank and it was lightning fast.

Then they stopped.

See, banking crisis over!

Except, it’s not.

It was just put on the shelf because they needed time to pass.

They needed people to forget about that crisis.

They also needed time to roll out FedNow and their CBDCs.

Then they pull the banking crisis back off the shelf, run that same playbook except this time it’s bigger….much bigger.

Wipe out all the small banks, all the credit unions, or at least wipe out enough that they rest will slowly die off over time.

You roll those small banks into JP Morgan Chase, Citi, BOA and Wells Fargo.

Then you have essentially only four banks remaining.

Then what do you do?

Then you wait some more.

Then you get those 4 down to 1.

Then when you only have 1 national bank left, you slowly merge that bank with The Fed until you have completed the plan.

These people think in 100 year blocks of time, not months.

They’ve been working this since 1913, and they’re ready to finish up the final act.

So there you go.

It’s not pretty, but what I’m telling you IS their plan.

Now, let me back it up and give you a lot more.

Start here and tell me if this sounds EXACTLY like what I just told you:

When you know…

YOU KNOW#FEDNOW https://t.co/qpQLzYDCTA

— Chad Steingraber (@ChadSteingraber) June 26, 2023

Testing complete….

And gee, what are the names listed here?

Are those the same names I just told you?

NEW: JPMorgan Chase, Bank of New York Mellon, US Bancorp and Wells Fargo, have completed formal testing for FedNow 😮

They will be ready to provide instant payments after the new service is live in late July 👀 pic.twitter.com/QqCWk98HL5

— Bitcoin News (@BitcoinNewsCom) July 1, 2023

Want a prime source?

Does Reuters work for you?

Fed says 57 firms set to use 'FedNow' instant payments after late July launch https://t.co/Absz0WxMwK

— DJ Peter Vas (35k) (@PeterVas6) July 1, 2023

From Reuters:

The U.S. Federal Reserve announced on Thursday that 57 firms have been certified to utilize its “FedNow” instant payments system after it launches in late July.

The Fed did not provide a specific date for the launch, but 41 banks and 15 service providers, including large firms like JPMorgan Chase (JPM.N), Bank of New York Mellon (BK.N), US Bancorp (USB.N) and Wells Fargo (WFC.N), have completed formal testing and will be ready to provide instant payments after the new service is live.

Jim Rickards has been one of the loudest voices sounding the alarm:

#Rickards stated that a #CBDC would facilitate "the creation of a social credit system that allows governments to punish those who engage in unapproved activity." https://t.co/UddLzcukV1

— Bitcoin.com News (@BTCTN) June 26, 2023

From Bitcoin.com:

Jim Rickards, an economist with more than 40 years of experience in investment banking, has warned about a hypothetical social credit system in the U.S. powered by a central bank digital currency (CBDC). In his latest article, Rickards explains that issuing a CBDC would allow the government to get the data needed to construct such a system.

Rickards stated that the information collected by monitoring transactions on a CBDC would facilitate “the creation of a social credit system that allows governments to punish those who engage in unapproved activity such as buying guns, donating money to the wrong political party, buying unapproved literature, etc.”

While recognizing this might sound paranoid to some, Rickards compares these measures to the ones taken by the federal government to stop the Covid pandemic, declaring:

Before the pandemic, you probably wouldn’t have thought that any of this was possible. But it all happened. When you think of it in that light, you begin to understand that some type of social credit system in the U.S. really isn’t that far-fetched.

A System Built for Control

In Rickards’ hypothetical system, implementing a CBDC would allow the government to control or block people’s movement to other cities or countries, limit their liberties by nullifying their opinions on social media, and even target them via intelligence agencies. Using the CBDC would be the only way of paying, and a social credit score would be the tool for limiting these actions.

According to his forecast, this might be done deceptively, establishing measures to pursue extremists and criminals first. On this, he declared:

It’ll all be made to sound very benign, even necessary, to support ‘our democracy’ against MAGA types, white supremacists, climate deniers and domestic terrorists.

More from Rickards:

https://www.youtube.com/watch?app=desktop&v=vu_-1CEAljk

One more:

https://www.youtube.com/watch?v=CeRJFUa75B0

In fact, Rickards has been telling us about “Ice9” for years:

MORE:

URGENT: FedNow Launching In July — Goodbye Freedom!

Have you heard of “FedNow”?

We’ve been talking about it but it’s not getting much attention in the MSM.

Of course not….

Want to know why?

Because it’s going to be very bad for you (and me).

This is a plan that goes back decades, even over a century….back to the launch of the Federal Reserve in 1913.

Watch this video I just found which shows EXACTLY what’s coming next and how you can be prepared for it.

Not much time left:

Now let’s go deep into the details and examine U.S. Docket No. OP-1670…

U.S. Govt. Docket No. OP–1670 Gives The FED Power to Seize Control of U.S. Bank Accounts! Do THIS Now…

WARNING: the U.S. banking crisis is NOT over.

Far from it.

Do NOT take your eye off the ball.

Here’s the truth…

If you use a checking account connected to the U.S. banking system, you could soon be at risk for surveillance of all your transactions, or worse …Direct control of your money by unelected officials in the U.S. government.

An economic forecaster and banking expert, who has been accurately predicting market disasters for more than four decades, is about to expose these disturbing details.

He correctly predicted the bank failures of the 1980s … the dot-com bust of the early 2000s … and the Great Financial Crisis of 2008.

In fact, his firm predicted bank failures months before the 2008 meltdown with a stunning 99.8% accuracy.

Those who listened to his warnings could have kept their money safe and even made substantial profits during each crisis …

While nearly all those who didn’t listen to him and failed to get out in time, suffered stomach-wrenching losses.

The Wall Street Journal reported that investors who followed his independent stock ratings could have made more money than if they had followed the ratings issued by …

Deutsche Bank …

Merrill Lynch …

JPMorgan Chase …

Goldman Sachs …

Standard & Poor’s, and …

Every single other firm reviewed in The Wall Street Journal.

In 41 seconds, he’s coming forward with a new warning, but it isn’t about the stock market.

It’s about your checking account — and how your financial transactions are going to be recorded and possibly even controlled by a small group of insiders in the U.S. government …

Starting as soon as June 2023.

The facts you’re about to hear could upset you. We urge you not to panic because, according to this legendary economic forecaster, there are four actions you can take to preserve and even grow your wealth.

You will hear about them in his presentation.

This man’s name is Dr. Martin Weiss.

After avoiding the spotlight for several years, he’s going public to reveal this new financial threat.

He will show you the actual document produced by the government, detailing their plan.

He will even reveal a top-secret presentation that the government used to train their agents to spy on us.

And he will show you how to protect yourself.

Now, here’s Dr. Martin Weiss …

Imagine a government agent gets assigned to snoop through your bank account — to see if your transactions are considered a “threat” to the government’s agenda.

If that idea sickens you … or if you think it won’t be a real possibility starting just a few months from today …

Then pay attention to what I reveal now.

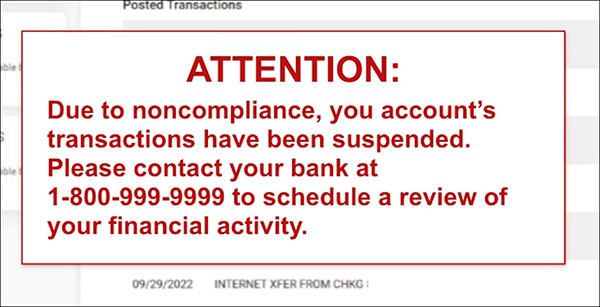

Because, according to this official government document I’m holding in my hand, starting as soon as June 2023, you could wake up one morning, log into your bank account and …

Stare at a red flashing alert that your account’s transactions have been frozen.

Your ability to send money and receive money — frozen.

Your crime? You didn’t commit one.

It’s all because of the U.S. government’s horrifying new program that gives unelected officials the power to closely monitor or even freeze your account based on your behavior, and potentially even based on your political views.

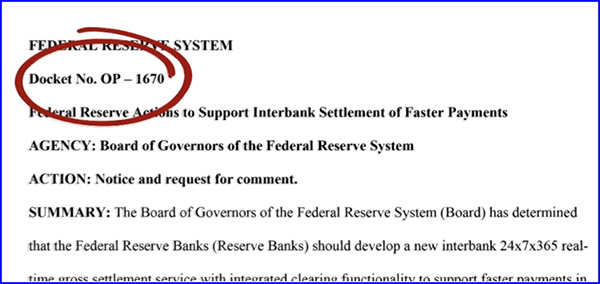

It starts with this 93-page government document.

Its name: Docket No. OP — 1670.

This innocent-sounding document, which was never meant for the general public, gives them the power to suspend your ability to pay others or get paid, even punish you with fees andfines, andultimately …

Seize control over your money.

Some of the largest U.S. banks are already joining our central bank, the Federal Reserve, to roll this out as rapidly as possible.

There’s a good chance your bank is already participating. I’ll give you the names of these banks in just a moment because …

There’s no stopping this from happening.

You don’t get a vote. You don’t get to “opt out.” And your money is in danger, unless you take …

Four Simple Steps to Protect Your Savings

The catch is …

You don’t have much time left.

We’re very close to the day when the government will roll out this new system.

They’ve already been caught red-handed snooping in the private emails and personal family videos of millions of innocent Americans.

Now comes the next layer of control.

And this time it’s for your money.

The Federal Reserve has set a date for when banks will begin handing over this control. It could start as soon as June 2023.

Fast forward to a future date and picture this:

You see a post on Facebook criticizing politicians for out-of-control inflation. You hit the “Like” button.

An hour later, you read a post by a blogger you follow, asking for donations.

You decide to give him $30 using PayPal.

When you click the button to send, a strange error message pops up. You figure the charity just didn’t set up their page properly. So, you move on and you don’t think anything of it.

But the next morning, when you log in to your bank account, you see this:

What the heck …!

You take fast, shallow breaths and your heart starts thumping quicker as you realize what’s going to happen.

Your electric bill is still due in a few days.

Your mortgage payment is set to draft from your account in a week.

And you had planned to use your credit or debit card to buy holiday gifts for your grandkids.

But now with your account frozen …

You’re helpless.

As your forehead breaks out in sweat, you call the number flashing on your bank account screen. Nobody picks up.

Instead, you get an automated menu that asks for your Social Security number and other sensitive information.

You never get to speak to a live person. A robotic voice makes you choose a date for a hearing to get your banking reinstated. The soonest appointment is over a month away.

After you hang up, the screen of your frozen bank account still stares at you.

How could this have happened?

You think back to what you’ve posted on social media. You remember the charities you’ve given to. The causes you’ve supported. You remember that the news has reported more and more men and women are getting “cancelled” by their financial institutions.

Why?

Did they buy too much gas? Did they donate money to the “wrong” candidate?

No one seems to know for sure.

But somehow, whenever you thought about protecting your savings from their control, you just shrugged your shoulders and figured you’d “get around to it.”

Now that your account’s frozen and it’s not coming back for weeks, you start to wonder:

What’s going to happen next?

Will the electric company send out a warning notice?

Or maybe they’ll just shut your power off.

And what about your mortgage?

How long before you start getting warnings about THAT?

How are you going to explain to your spouse that you need to stop all spending from your checking account?

You can’t write checks. You can’t pay off credit cards.

This might sound like a nightmare straight out of a dystopian novel, but …

As you’ll see in just a couple of minutes, millions of innocent American citizens have been spied upon by the government. Quite a few have also had their accounts suspended.

In fact, government confiscation of personal assets has happened a lot more frequently than most people realize. Right here in America.

So, government surveillance and manipulation of financial transactions would be entirely new.

It would simply be the NEXT step in a very disturbing pattern.

And the Federal Reserve’s Docket No. OP — 1670 shows how that would work.

The document maps out how a small group of unelected government officials will soon gain access to all your financial transactions.

And we know, from years of experience, that government ACCESS to all your data is just one step away from the government’s power to CONTROL everything that data tells them about who you are and what you do.

They’d have the power to watch how you invest your money, and …

Restrict the amount you invest in companies that are not “compliant” with environmental, social and governance standards.

They’d have the power to limit your purchases of fossil fuels, including gas at the pump.

They’d have the power to restrict your contributions to certain causes or political parties.

They’d have the power to pressure folks of all ages to get government-mandated vaccinations.

Or worse.

If you find this hard to believe, just consider what our government has already done.

In 2013, the National Security Agency (the NSA) illegally collected the phone records of millions of American citizens.

Not just once, but for over five years.

The government spied on millions of people who were never suspected of any wrongdoing whatsoever.

That’s not all. The NSA and the FBI colluded with America’s biggest tech companies to spy on nearly everything you could do online.

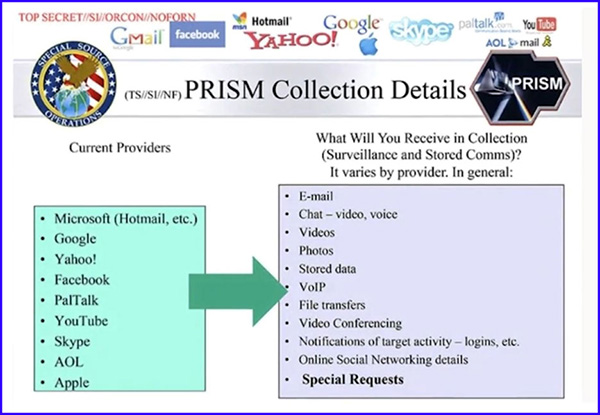

It’s all revealed in this slide from a top-secret PowerPoint presentation that the NSA and the FBI used to train their agents:

Look at the left column. These are the so-called “providers,” the companies that provided your private data to the government:

Microsoft, Google, Yahoo!, Facebook, YouTube, Skype, AOL, Apple, and others.

And see this list in the right column? Those are your private activities that the government agents could search and spy on at any time, whether live or recorded.

Your chats.

Join the conversation!

Please share your thoughts about this article below. We value your opinions, and would love to see you add to the discussion!